I'm doing an inner victory dance right now. I can't do an actual victory dance because it's too damn hot right now. But that's o.k. because the 401k check finally came and I now have enough money to pay off the balance of my credit card! The check couldn't have come more last minute. Today was literally the last mail day before my flight for Thailand and I have been sweating bullets (literally and figuratively) hoping that check would arrive before I leave the country.

I'm not sad to say that I'll be closing a chapter of my life. It's been about 5 years since I got myself into this mess and I've spent the last 2 years toiling to pay off the approximately $30,000 in debt I had accumulated while I was in college. All the sacrifices were worth it. The bad haircuts. The scant wardrobe. The peanut butter and jelly sandwiches. The terrible job. I never want to do that again!

This whole experience has made me appreciate everything so much more. I was trying to think of exactly what it is that I appreciate more but I really think it is EVERYTHING. I appreciate not having to worry about money and all the things that I learned you can enjoy without money. I appreciate how I learned who my true friends are and how you can pretty accurately judge a person based on how they treat people who don't wear fancy clothes or flash their money around. I appreciate the freedom that comes when you don't have to struggle paycheck to paycheck to survive. I truly appreciate all the things that you can buy with money because I lived so long without having much.

Tomorrow before I go to the airport I'm going to go to the bank to deposit the check. It's strange how the timing worked. Depositing the check will be one of the last things I do in the States and then I'm off to start a new life thousands of miles away. It's the rebirth of me. Weeee!

Don't forget you can check out my new blog, Living in Thailand, to follow up on my progress.

Saturday, July 22, 2006

Hallelujah, debt salvation has come!

Monday, July 17, 2006

New blog is up!

In case you were interested in following my adventures of living in Thailand, the new blog is up. I'll be leaving next week and hopefully I'll be able to start posting soon after I arrive (depending upon the availability of the internet).

I'm still not debt free. I've been waiting to receive my check for the 401k distribution for a week now. I called them today to see if they had sent it and found out they had sent it to the wrong address (they put the wrong apartment number on it). After arguing with them for a while that I would not get it if they sent it to the wrong address (they thought it would magically be forwarded to the correct address) they cancelled the check and said they would send another one. Unfortunatly, by the time they get around to sending me the check I'll be out of the country anyways so I'll have to get someone else to deposit it for me. I guess no one said moving out of the country would be easy.

Thanks to everyone for all of your support and ideas and suggestions. I might keep posting here from time to time but it will most likely be to talk about travel and related expenses and ways to save money while living abroad. If you are in the same boat as I was two years ago, you might want to check through the archives for ideas and inspiration to pay off your own debt.

Happy debt defying!

Friday, July 07, 2006

Waiting...Waiting

My life is in limbo right now, just waiting to leave for Thailand. I'm not working right now so I have loads of free time. Some people might complain of boredom but I have to say that I could really get used to this whole not having to work thing. I feel like I actually have time to do stuff like read and go to the gym. That stuff is normally neglected when I have a job because I'd rather veg out and relax after working all day.

I must say though that moving to another country is a job in itself. There are so many things that you have to do before you leave because you can't do them once you are gone. For example, yesterday I had to go and get my immunizations at the health clinic. Luckily, my friend's mom told me where to go to get them for cheap because it could have cost a lot of money. For her, even with insurance her doctor was going to charge her $800 for all the shots she needed. The clinic only charged $90. Although its not required to get the shots before you go, I think the $90 is worth reducing my chances of getting some crazy disease.

I also had to set up a new bank account with Citibank because they are the only bank I know of that has branches and ATMs in Thailand. It would suck to have to pay the ATM fee everytime I had to take out money. And now I can sign up for their savings account which pays 5% APY. Not only does it pay a higher interest rate than ING Direct, but your checking and savings accounts are linked so you can instantly the money you don't need immediate access to so it is earning interest for you. Luckily, I had no problems signing up with them (unlike all the drama I experienced signing up with HSBC).

I'm struggling with the decision to sell my car. Part of me wants to sell it because I would have extra cash and I would be able to pay off my student loans. But the other part of me is telling me not to sell it because if things don't work out in Thailand I would have to come back and buy another car and pay taxes and license and all that good stuff again. Having the car would give me a sense of security while I'm in Thailand that if things don't work out, I can always come back home and start over again without much hassle. The extra money would be nice though.

I'm so excited to get going. My 401k check should be in the mail on Monday so I'll have the money to either pay off my debt or buy my plane ticket (depending on what I decide to do with my car). Until then, I'll just have to keep waiting!

Tuesday, June 27, 2006

Want to save $20,000 in a year?

English teachers abroad are in very high demand and just by being a native English speaker you are qualified to get some pretty high-paying jobs in foreign countries like Thailand, Korea and China. I say high-paying because while they may not be as much as you can make in the States, the cost of living in these countries is extremeley low. Even if your income was about $30,000 you could get by easily on $10,000 a year, especially if they provide you with housing. You can command even more money if you have a TESOL certification and can make money on the side working as a private English tutor.

Not only will you be able to save up money but you'll be able to experience another culture first-hand. You can never truly grasp a country in 1-2 weeks while on vacation and you never get below the surface of the tourist traps to see how people really live. Plus you won't have to go away on vacation because there will be plenty of exciting places to explore in your new home.

Living abroad is probably not for everyone. You'll most likely have to live without a lot of the creature comforts that we take for granted in the States like huge living spaces and air conditioning wherever you go, but once you live without them for a while you realize that you don't really need them and you appreciate them a lot more when you do have them.

I most likely won't be able to save up loads of cash while I'm living abroad because I plan on doing a lot of traveling around Asia but the good thing is I won't have to go into debt to it!

Sunday, June 25, 2006

Selling my soul at a garage sale

Yesterday my friend and I had a garage sale to get rid of as much stuff as we possibly could before we move to Thailand. I've never been much of a garage-saler, mostly because I am never up early enough to make it to them on the weekends. I knew people would be cheap and would try to haggle, but I wasn't quite prepared for the extent of people's audacity for bargaining.

First of all, I set off going around my apartment thinking that I would get rid of nearly everything so that all my material belongings would be able to fit into one suitcase. I soon found out that parting with things was harder than I imagined. Things that I hardly noticed on a daily basis took on a sudden sentimental value. I vowed to be strong despite my over-emotional reactions because I figured it would be worth the temporary pain to be divorced from any material longings.

So I show up and put my whole life on display. I figured people would be quite impressed. I was selling some nice stuff, some stuff was practically new, never been used and of course, I bought it so it was of the highest quality. Boy was I wrong. There is something infuriating and humbling to see someone pick through your belongings and see them turn up their nose at it. Or when someone asks you how much you want for something and you say $1 and they put it back down and walk away. What? Was $1 too much for you? I paid $20 for that thing! Were they expecting that I would say, "Free for you!" You can't buy anything for $1 anyways. Even a pack of gum costs more than $1!

I never got the whole bargaining thing down either. I would try to start off high expecting them to counter offer and they would just walk away. And if I started low they would try and haggle. This one lady came up with her arms full of stuff and offered me $4 for it all! She must have lost her mind. I thought well I'll try and haggle because I needed to get rid of the stuff anyways so I countered with $7. A whoppin $3 more and she looked at me like I was crazy and said "I said $4." I was tempted to tell her to stop wasting my air and get out of my face, but I decided to take the polite route and told her that her offer was too low. For that amount of money, I would rather donate it to the Goodwill so that the money will go to a good cause instead of some cheap rich lady who's husband was waiting for her in their nice car with the engine running.

I ended up making nearly $60 which isn't bad because nobody bought the major stuff I was selling. And to be honest I don't even remember what I sold. The rest of the stuff will probably end up at the good will, hopefully to homes that will get some good use out of them. And the extra $60 will go to payoff the debt and/or my savings account!

Friday, June 23, 2006

More surprises up my sleeve

I made a big decision. To celebrate getting out of debt I'm going to make a drastic change. I'm moving to Thailand to teach English. I've already been offered a job there at a private school and a good friend of mine will also be teaching at the school with me. I'm very excited about the change.

It seems like now would be the perfect time to do something like this. I'll be debt free, I'm just getting out of a long relationship and I have no job so I have no obligations to keep me here. I'm young and have no mortgage and I'm in good health and adventurous. How many times in my life will I be this free?

I did some calculations and decided to make a major personal finance faux pas: I'm going to cash out my 401k to pay off the remainder of my debt. I guess Henry's comments were right; once you start toying with the idea it's hard to give up. I'll have to pay the 10% penalty and taxes but I figure I'll have to pay taxes when I retire anyways and the 10% is worth the peace of mind of not having debt hanging over my head anymore.

I'll also be selling my car when I move so that will give me enough money to pay off my student loans and have a couple thousand left over for emergency money. I'll be completely debt free, no credit cards and no student loans and with money in the bank. I didn't think that would be possible for another couple of years. I'll also be selling my portion of the furniture to my ex-boyfriend and I'm selling all my books and DVDs on Half.com. Everything that I own will soon be able to fit into a couple of suitcases.

After being in debt for so long and having material possessions tie me down, it'll be an interesting experience to live without any of those constraints. For me, the whole point of getting out of debt was to be able to experience freedom again. The freedom to go where I want to go and do what I want to do and to have freedom from any worries about things.

For example, a couple of weeks ago someone hit my car and left a scratch on my bumper. I was so mad that someone could hit my car and not leave a note. I was angry because I would then have to either fix it or just accept the loss. It sounds silly but when you have things you always have to worry about them breaking or getting lost or having to replace them. I want to be in a place where none of that matters.

I probably won't move until mid-August so I'll have enough time to take care of all the loose ends. I'm not sure how accessible the internet will be but I'm hoping to continue to blog, probably not solely about personal finance but also about my travels and experiences in Thailand!

Tuesday, June 20, 2006

Gambling isn't for me

Yes, I know it's been a while since my last blog posting. I admit I've been going through a blog funk, mostly because life has been hectic and I've been frustrated with the pace of the debt payoff. The smaller it becomes the more impatient I become to get rid of it. It's changed from a giant menancing dragon into a tiny pestering fly in comparison which I'm happy about but I just wish I had a fly swatter that would make it go away NOW. :)

The new job took a dive for the worse. I took a gamble even taking the job and that gamble isn't going to pay out. I knew it was 50/50 going into the mortgage business now because rates are going up and a lot of places were struggling as business was drying up but the promise for greater pay was too alluring to pass up. Unfortunately, I think the promises were too inflated so I'm going to start looking for another job. It's a bummer because it throws another wrench into the debt reduction plan but hopefully another job will come along, this time a stable, normal job.

I was contemplating cashing in my 401k to pay off my credit card just so that it would be gone and done with. I have about $4,000 in the 401k and I think after paying taxes and the penalty I would have just enough to pay off the rest of my debt. I know, I can already feel the angry comments being hurled at me. I'm not going to do it, but it's tempting! The thought of not having any more credit card debt makes me tingle a little.

I'm going to do something I have never done in the history of this blog. I've added a Paypal donation button. If you've enjoyed reading my site AND feel it's a worthy cause AND you are in the financial position to do so, you can make a small donation to help me get out of debt. I've avoided adding these types of links to the blog in the past because I'm definitely not looking for a handout. Don't donate because you feel obligated or anything like that, only do so if maybe I've made you laugh or gave you something entertaining to read while you were at work or you've been following my story from day one and are as excited as I am to see me get out of debt. Of course, all of it will go directly to paying down the evil credit card.

Soon people, soon. Only $2,150 to go. It's so close but farther away than I would like.

Tuesday, June 06, 2006

I'm a Carnival Flake

Umm, oops? I signed up to host the Carnival of Debt Reduction a couple of months ago and totally forgot about it until I saw Mighty Bargain Hunter's post about the carnival. At first I thought he had gone nuts but then I realized that no, I'm really just a Carnival Flake. My apologies to all! But check out MBH and the posts he's selected for this week.

I'll ban myself from hosting carnivals from now on. :)

The debt reduction has reached a snail's pace but I'm still trying to make progress towards my goal. Soon, very soon, I will be able to say that I'm free from credit card debt.

I finally received my pin number from HSBC but I refuse to transfer any money to this account. The 0% interest balance transfer game is tricky business and the last thing I need is for HSBC to mess something up and cost me a lot of money. I made $90 in interest last month from the money I borrowed from my credit card at 0%. It feels good, like I am recouping some of the money I have paid them in interest over the years. But I must caution that I wouldn't recommend it to everyone. You must be extra vigilant to make sure that all of your bills are paid on time or they could spike your interest to some ridiculous amount and you'll be in a bad position.

On another note, if you haven't seen it yet you should check out the movie,The Inconvenient Truth. It might not necessarily be directly related to debt reduction or personal finance but it will make you think twice about the consequences of consumption and material excess. If financial freedom, peace of mind and a comfortable retirement doesn't motivate you to save your money and stop buying "things," perhaps the end of the world might give you the impetus to reconsider your spending habits? I kid, I kid. Kind of.

The website also has some eco-friendly money saving tips. Check it out.

Tuesday, May 30, 2006

Deep Fried Cars

Forget the Prius or the Insight or the Honda Civic hybrids. I want my alternative fuel car to run on vegetable oil, the kind that you use to deep fry twinkies and onion rings (what you've never had a deep-fried twinkie?).

My grandma, always the first to know of the latest technological innovations, told me she had heard about a company that was selling kits to convert your car so that it could run on vegetable oil for only $800. I did a quick search on google and found the website she was talking about.

The company, Greasecar, sells a self-install kit that converts your car to run on plain old vegetable oil. You don't even have to pay for the vegetable oil because most restaurants have to pay a disposal fee to get rid of the vegetable oil they use for frying. If you could find a good local restaurant that uses lots of cooking oil, you could convince them to give it to you for free to save them the hassle and all you would have to do is filter the oil. Assuming that you pay $100 in gas a month, the kit would pay for itself in 8 months.

I was almost ready to buy the kit when I realized that the kit can only be installed on diesel engine cars. Boooo! I knew I should have bought the diesel Jetta!

Most diesel cars available in the U.S. are either older models Mercedes, big pick up trucks, or newer Volkswagens. I definitely don't want an older car that will have to be in the shop all of the time, I am not necessarily a pick-up truck kind of gal, and even though I already own a Volkswagen, I don't think I could trade in my Jetta for a diesel version without acquiring more debt.

My deep fried car project will have to wait for now but as soon as I get out of debt and I have some savings, I'll be looking to trade my car for a car that will relieve me from being at the mercy of gas prices. And gas prices aside, wouldn't it be cool to tell people your car runs on cooking oil?

Wednesday, May 24, 2006

Sticker Shock

Against my own advice, I ventured into the murky depths of the mall today. I normally try to stay as far away from them as I possibly can but I suffered from a temporary lapse in judgement. First of all, I was searching for a birthday present and thought if I could walk around the mall I might get some ideas on what to buy. Second of all, my clothes have started to get that too-tight look that means that my body is expanding against my will. It is a sick cruel joke my body plays on me; every time I try to lose weight I end up gaining weight. Maybe I should try to gain weight in order to lose weight? And, it has been ages since my last hair cut and I felt the need to splurge on a nice cut and color.

The good news is that even though I went to the mall with every intention of spending money, when I looked at the price tags I almost fell to the floor in shock.

"HOLY bejezus, $130 for a pair of jeans???"

"$40 for foundation makeup? $28 for blush? Bless their souls; they have lost their damn minds!"

"They want me to pay how much for this serving tray? That must be $9, not $90."

These were my inwards conversations as I made my way through the mall, just aching to spend some money but not quite THAT much money.

The worst was when I went to go get my haircut. I had bargained on about $150 for a cut and color. Boy, was I ever wrong. Thank goodness I asked before I took a seat in the chair! Apparently, haircuts at this salon run from $85 for a "Stylist" to $135 for a "Creative Director" and anywhere from $145 to $205 for a color. I tried to maintain my calm and composure while she was explaining their pricing, and as soon as she looked away I ran as fast as I could.

Have I really been not shopping for that long? When did everything get so expensive????

Sunday, May 21, 2006

More HSBC Drama

Let me just clarify a few things in regards to HSBC. I misread the FAQ's on the HSBC site in regards to the fees for bank transfers. This is what their site says:

*No transaction fees if you transfer money into your HSBC accounts from your non-HSBC accounts

*A $3.00 transaction fee will be charged for each outbound transfer from your HSBC accounts to your non-HSBC accounts

At that point I had stopped reading because I was ranting and raving about the $3 fee. If I had maintained my compusure and continued reading the line below, I would have seen this:

*No transaction fees will be charged for HSBC OnlineSavings, Domestic Private Banking or HSBC Premier customers .

Now, tell me, does it make sense to have this on a whole separate line. If I were writing these FAQs I would have written it like this:

A $3.00 transaction fee will be charged for each outbound transfer from your HSBC accounts to your non-HSBC accounts (No transaction fees will be charged for HSBC OnlineSavings, Domestic Private Banking or HSBC Premier customers ).

This would imply that the 2nd and 3rd bullet points are related. Or better yet:

A $3.00 transaction fee will be charged for each outbound transfer from your HSBC accounts to your non-HSBC accounts*

And then a little note at the bottom explaining the conditions of who pays and who does not. I mean, its really not that important but it would have saved me the heart attack.

In other HSBC news, I still have not received the PIN number they were supposed to send me a month ago. I called them again to see what the deal was and of course, it was more drama. After explaining to them that I had not received the PIN and that they had sent it to the wrong place before he said that he could not send me another PIN number because I recently had a change of address. "UMMM? No, I never changed my address. You merely sent it to the wrong address before." He said yes, he could see that in my file but that he couldn't send it to me because of the problem and I would have to fill out some form and fax it back to them to request a PIN change. At this point, I lost it. I normally try to be a courteous calm and collected person but if I have to call any customer service place 3 times to solve a problem, my nerves get worn a little bit thin.

So after explaining to him that I didn't have time for this nonsense I told him I would simply like to cancel my account. He then informed me that I could cancel my account if I would like, but since I had not had my account for more than 6 months I would be charged $25 to close the account. My pissed-o-meter was through the roof at that point and I told him that I wanted to talk to his boss. He insisted that his boss wasn't going to tell me anything different and that it would be a waste of my time to talk to him. Of course, I insisted on talking to him anyways and after waiting on hold for 5 more minutes his boss came on the line and told me he would overwrite the system so that a new PIN would be sent to me.

Now, let me ask you this. Why do I always have to be at my breaking point before they figure out how to solve a problem, i.e. the lady that told me there was no way I could fix my user name and password until I received my PIN until I insisted that she fix it and this turdball who insisted there was no way for me to get a new PIN without filling out some form and faxing it back to them. I don't like to be that crazy lunatic customer but by golly if they aren't going to get it done without me losing my cool, then thats not my problem.

We'll see if I stick with HSBC or not. At this point I have so much time and energy invested into this process that I might as well take advantage of the higher interest rates that they are offering. Both ING and HSBC raised their rates but HSBC's are still .5% higher than ING's but I have become quite attached to my drama-less banking at ING.

Thursday, May 18, 2006

Why ING is Better than HSBC

I've had my ING Direct account for more than a year now and have never had any problems with them. The sign up process was painless, when I have questions their customer service is awesome and their online site is easy to use. The only reservation that I had with ING was that some of its competitors were paying higher interest rates on their savings account. For example, right now ING's rate is at 4.15% while HSBC is at 4.5%.

I decided to at least give HSBC a try. The application itself was fairly easy but unlike ING, you have to wait for them to send you your user ID and password in the mail. I signed up for my account and waited and waited and waited. Finally, after about a month of signing up I called them and asked them what the deal was. I know I could have called earlier but I am a busy lady, like most people, and just never had the time to call them. So on a Saturday afternoon I called them and the customer rep informed me that they had forgotten to put my apartment number on the mail. AGH. That was a little irritating but what was even more irritating was that he wanted me to call back on Monday to ask them to send it to me again.

This kind of thing rubs me the wrong way. I have no idea why he couldn't just do it over the phone right then. Do people who work on Monday have special mail rights that people who work on Saturday do not have?

So after wasting even more of my time to get the problem fixed they finally sent me the info I needed. BUT when I went to log into my account the password and user name did not work. Frustrated, I called the customer support and after waiting on hold for 15 minutes I tried to explain to the customer service rep that the password and user name that they sent me did not work. She said there was nothing she could do for me and that I would have to change my password online using my PIN number. I explained to her that I had not received my PIN number (and still 3 days later I have not received it) and that I couldn't do that. She said I would just have to wait for it to come and after a few minutes of me trying to explain to her that I was entering in EXACTLY the user name and password THEY sent me and that it didn't work she put me on hold. When she came back she asked me to try it again and MIRACULOUSLY it worked.

I was relieved and perturbed at the same time. She offered no explanation of why all of a sudden it worked after she told me over and over again that she couldn't help me. If I had not argued with her I would still be waiting to be able to sign into my account and access my money. Luckily I only started off with $20 for this exact reason.

After I was able to log in I noticed that there was no way to transfer money between non-HSBC accounts. I had already given them my routing number to my checking account so I thought I could easily transfer money back and forth between the two, like with ING. Noooo, that is an additional service that you have to sign up for. Transfers going into your account are free but any transfer going out of your account is charged a $3.00 processing fee. I guess I had been so spoiled with ING that this came as a shock to me.

So far, everything with HSBC has been a problem. Don't you sometimes wish that you can send people bills for the time they have wasted in your life? Instead, I'll have to pay the $3 to take my $20 and put it back into my ING account.

Thursday, May 11, 2006

Pay Day Advances

Today I was hit up by someone wanting to put an ad on my site. Normally, this would be a great thing because hey, if I can sell advertising space on this blog then I can pay off the debt even faster, right? But when I checked out the site I thought to myself that these people must be delusional or on crack to think that I would ever link to them on my site.

I'm not going to say who they are, but they were one of the many pay day advance companies that rip people off when they are probably already in a bad financial situation to begin with. Let's say you are behind on your bills and don't get paid for another week. You need cash NOW so you find one of these cash advance places that will give you the cash you need now. Nice of them huh? There's only one small catch: they will charge a teeny weeny amount of interest, in this case an APR of 391%. No, not 3.91%. Three hundred ninety one percent.

Holy moses! 391% APR? Are they out of their minds? Why not just ask them to give up their first born child?

At first when I looked at the site they said you can get up to $500 in your account tomorrow for only $15 per $100 borrowed*. "Not terrible" I think to myself, "but ahh, what is this * about?" I read down in the small print that finance charges are calculated every 14 days which is equivalent to a 391.07% APR. Very tricky bastards!

It makes me sick to think of paying that much interest. And think about it. If you are already hard up for cash before you get paid, when you do get paid you will have to pay back that loan and your next paycheck is already gone. Then what do you do? Take out another pay day loan? It would be like being in a never ending cycle of debt, digging a deeper and deeper hole that you will never be able to get out of.

So just don't do it! I know I am probably preaching to the choir here but people should avoid pay day loans like they are the plague. If you need cash, ask a friend. Do a balance transfer. Get another job. But whatever you do, don't get a pay day loan!

Thursday, May 04, 2006

Free brain food

I randomly came across this site on Wikipedia, ThoughAudio.com. They offer free MP3 downloads of classic books ranging from Plato, to Ayn Rand to Sun Tzu. I was subscribing to Audible but canceled my subscription because I wasn't commuting to work anymore. I started missing the service because I do listen to the books from time to time when I work out or when I go to sleep at night, but now there are tons of books I can listen to for free! Hooray!

Also, if you were looking for free ebooks, there are lots of books available from the Project Gutenberg. I personally don't like to read books from a computer but it's fun to know it's there. I'll probably still just go to the library and get the books, for free!

Tuesday, May 02, 2006

Paper or Plastic? I Say Neither!

The other day I splurged and made a big purchase: two canvas grocery shopping bags for $2.50 each. I had gotten so annoyed with the huge pile of plastic and paper grocery bags accumulating under my sink. I must have a stash under there that would last me for years to come but I just can't throw them away because I feel like that is such a waste. So after thinking about it for a while I took the plunge and made the $5 purchase.

Today I took them to the store (Trader Joe's) and was pleasantly surprised to learn that every time you bring your own bags to the store, whether they be bags from a previous trip or the canvas reusable ones that I had, they will enter your name into a monthly raffle for a $25 gift certificate. I'm crossing my fingers that I win.

So far, here are my advantages:

1) No more messy bags under my kitchen sink.

2) Chance to win free food.

3) Reducing waste and pollution.

I was doing a little research on the environmental effects of paper and plastic bags as opposed to using reusable bags and found this on the EPA website:

"* In New York City alone, one less grocery bag per person per year would reduce waste by five million pounds and save $250,000 in disposal costs.

* When one ton of paper bags is reused or recycled, three cubic meters of landfill space is saved and 13 - 17 trees are spared! In 1997, 955,000 tons of paper bags were used in the United States.

* When one ton of plastic bags is reused or recycled, the energy equivalent of 11 barrels of oil are saved.

Many grocery stores now offer for sale sturdy cloth grocery bags. Some of these stores even give you a little discount (e.g., five cents per bag) if you bring your own bag. So, keep a stash of reusable bags in your pantry or if you drive to the store simply keep them in your trunk."

Apparently, CostCo, Whole Foods and Ikea offer a $.05 to $.10 discounts per bag when you bring your own bags and of course Trader Joe's has the monthly raffle. Who knows, your local grocery store might have a discount too.

Friday, April 28, 2006

How saving the environment can help save you money

Nowadays, when I look at the gas prices I shiver in horror. I thought there was no way it could get any worse than $3 a gallon but now even the cheap stuff is close to $3.25 a gallon. I'm not alarmed by the gas prices because I drive a gas guzzling SUV or drive an excessive number of miles and part of me is glad that the higher gas prices are making people think about alternative forms of transportation and conservation (the operative word in that sentence being "think"). Maybe more people will go out and by hybrid cars, making the actual cost of hybrid cars go down. Maybe more people will take the bus so that they will actually start adding more buses to the route and lowering bus fare. And maybe more people will start riding their bikes and they will see the need to make more bike lanes on the street (you have to be pretty fearless to ride your bike in the street where I live). I'm not going to get into a lengthy debate about whether or not the gas prices are justified or not because, well, it just makes me angry.

But I do want to point out that it's not just the actual price we pay to fill up our tank of gas that will be going up, it will be the price of everything. Think about it. Transport costs go up. Electricity prices go up. The cost to manufacture goods goes up. As the cost to do business goes up, companies will pass this on to the consumers as higher prices. I'm no economist but I foresee inflation. Not just your regular run of the mill inflation, but big mean bad angry inflation (can you tell I am not an economist?).

They say that gas prices are the result of "supply and demand" in the market. So what can we do as consumers to decrease demand for energy therefore bringing the market cost back down and saving the environment in the process?

Well there is the obvious DRIVE LESS and buy more energy efficient vehicles but there are also a lot of other things that we can do that will save us money in the short term as well as reduce consumption. By reducing consumption we not only cut back on the amount of waste that is created when we throw the product away but also reduce the amount of energy and resources that it took to create it in the first place.

One of those things we can do is to stop buying bottled water. Bottled water is one of my biggest pet peeves. Not only are you paying a ridiculous premium for something that you can get right out of your faucet, but the waste it creates is astronomical.

PEOPLE, you have got to get over your fear of the water in the faucet and stop buying bottled water! What a waste. We don't live in Tijuana where it probably isn't safe to drink the water. Do you know anyone who has ever gotten sick from drinking the tap water? I certainly don't. Studies have shown that bottled water is the same if not worse than tap water. And if it's taste you're worried about, I have found that by purchasing a filter and keeping water in the refrigerator I end up with water that is virtually indistinguishable in flavor from any water I have had from a bottle. And if its portability you worry about, just buy a water bottle that you can wash and use over and over again.

I use the Brita Pitcher and Nalgene Water Bottle, both one time investments that have paid for themselves many times over because I don't need to constantly buy bottled water. If you consider that the price of a bottle of water is approximately $.50, the total cost of these two items is about the same as 80 bottles of water. Assuming that you drink two bottles of water per day, the cost of both of these items will be recovered in less than two months.

Have you ever thought about how much environmental harm is caused by those little water bottles? The Container Recycling Institute estimates that 1.5 million barrels of oil are consumed every year, just to transport bottled water in the United States. That is enough oil to fuel 100,000 cars for one year! That is not including the energy cost to produce the bottles or to transport the waste that will end up in landfills for more than 1,000 years, the time it takes for a single bottle to biodegrade.

Just by making one small change, you could be saving yourself money, reducing the demand for oil and saving the environment, all at once.

Ok, I'm going to go hug a tree now.

Wednesday, April 19, 2006

Vacation time!

I'm officially done with my last job and don't start my new job until May 1st so that means I have about 2 weeks of much needed vacation time. I would love to pick up and go on a road trip or small vacation but I still have my accounting class that I have to go to twice a week. That's o.k. though because it will help me not spend money on hotels or gas and I live in southern California where it shouldn't be hard to find fun things to do close by.

I got my last check yesterday so I am filthy rich. Well, not really but I am not sure what I should do with the money. All of my bills are paid for the next month and I have about $1,000 left over. I'll need to keep some money around for food and gas as well as other random expenses. Normally I would put any excess towards my credit card but I'm not sure when the next time I will see a paycheck will be. I think for the time being I will put the majority of it in my savings account and count it towards the debt reduction total and if for some reason I need it I will be able to still have access to the money. So don't panic if you see the debt totals rise. It doesn't mean that I've gone on a wild shopping spree with my credit card; it just means that I've had to dip into savings until my next paycheck at my new job.

In other news, I've decided to revive my failed attempts at making money off of the 0% balance transfer offers I receive all of the time. When I had tried this venture before I had received an offer for 0% interest on the balance transfer until a specific date. That is why it was so frustrating when they were taking their sweet time to transfer the money to me because every week they stalled I was losing out on the time I could be accruing interest on the money. Well last week I received another one of those offers in the mail except this time the offer was for 0% interest on the balance transfer for 6 billing cycles. I thought at least this way if they tried to delay the transfer, the time when I owed the money would be pushed back as well. The offer said I could do it all online so I logged onto my account and noticed another offer:

0% interest for 6 billing cycles and NO TRANSFER FEE

Woot! I was even more excited about this because that would save me $75 and make all of the money I earned as interest truly free money because it required no initial investment from me. But when I'm filling out the transfer form it asks me for the address of the bank. I wasn't sure what to put here. Could they mean the branch office? Or the corporate office? Or some other office address? So I call them and the customer service rep quickly says she can take care of the balance transfer for me. The catch is though that she doesn't show that the 0% interest for 6 billing cycles and no transfer fee offer is available to my account. Ummm, that's weird because I was looking at it on my computer screen at that very moment. She can't offer any explanation but says that I can call back later and ask them to waive the fee. I laugh at this because we all know that once the credit card companies have their claws in you there is no way they are going to go out of their way to make your life easier. So I decline and tell her I would rather do it all online where I can avoid paying the balance transfer fee at all. She pauses a moment and asks if she can put me on hold...I got all tingly because you know whenever they put you on hold they are simply pretending like they are going to ask their supervisor if they can do something "special" for you. Just as I suspected after a minute had passed she got back on the phone and said that she could waive the fee right then and there. Yeah!

I also decided to sign up for a savings account at HSBC because their rates are way higher than ING Direct. HSBC's rates are at 4.5% while ING is stuck at only 4%. I have had no problems with ING but a half a point of interest could mean as much as $10 more per month on my balance transfer.

Overall, I think it will be a good deal. I'll get to keep the money longer, I won't have to pay a balance transfer fee and I'll be earning at a higher interest rate. Overall I hope to earn $88 per month for 5 months all for doing nothing (except for taking a hit on my credit score for having a large amount of credit).

Monday, April 17, 2006

Book Review: Not Buying It

A while ago I was sent a reviewers copy of Not Buying It by Judith Levine. It took me forever to read, not because it was boring or tedious, but rather because the book covered so many interesting topics that I would read a page and be distracted by wanting to look up more information about that topic or look up a book that she mentioned. This book-induced ADD is a good indicator that whatever I am reading is thought provoking and inspiring.

I was almost turned off by the book because the beginning pages are filled with Bush bashing and liberal political rhetoric. While I am myself a liberal, I get turned off by overly zealous ideologues weaving in their political rhetoric at inappropriate times. I decided to keep reading (after all the book was free) and was glad that I did. The book not only chronicles her experience of a year without shopping but goes deeper into the anthropological, sociological and political forces behind shopping. "Not Buying It" explores the most banal questions, for example, "How essential are q-tips anyways?" to the more profound, "What environmental impact do my shopping habits have on the planet?"

Going a year without shopping is an interesting endeavor, however, it would have been much more interesting if she hadn't admitted to stocking up and binge shopping before January 1st and conveniently not counting the stuff that she buys for her home renovation or the generosity of her friends offering to buy her this or that or picking up the tab when they went out to dinner and the movies. At the point when my friend is paying for me whenever I go out with them, even though I have the money, I would have either stopped going out with them or chipped in my portion of the bill. I still give her kudos because she went much longer at not buying anything than I ever could.

Which makes me wonder, how long could I go without buying anything? I've contemplated doing my own experiment to see what it would be like to not buy anything and see how long I could last and how much money I could save. Then I realize that in essence, this is what I have been doing for the past two years while getting out of debt. I don't need any more severe deprivation to know what it will feel like, especially when I am so close to being out of debt now.

Do you think you could do it? How long do you think you could last?

Thursday, April 13, 2006

I got a new job!

What a relief! It's only been a week and already I've had two good job offers. It was not easy quitting my job without having another job lined up but I am glad I took the risk. I had known for a while that my job was not right for me but I just wasn't in the financial position to do anything about it. So finally, all the months of saving and paying off my credit card and transferring the remaining balance to a 0% card finally paid off! I had the freedom to quit when I knew it was time to move on and now I have a new job that I think will make me much happier and ultimately much wealthier.

The job that I am accepting was the result of a referral from a friend. The day that I quit she told me about the opportunity. It was great timing. I interviewed with two of the people from the office and got really excited about the job. It is in an awesome location a block away from the beach, a casual environment (the guy was wearing flip flops and jeans when I went to go see him), the people seem really nice and free of office politics and there will be lots of room to grow and learn and make lots of money.

The only problem is that I would be hired as an independent contractor without any benefits like health insurance. Initially I will be paid on salary and then slowly that would be phased out to a commission only basis. I know that this is risky but I feel that the time to take risks is now when I don't have any dependents or a mortgage or massive bills to worry about. I do have my credit card debt but I am confident that I will be able to pay it off before I have to start paying any interest on it.

I was offered another position that would be a more stable and secure corporate job. I weighed the benefits between the two jobs and came to the conclusion that I just wasn't made for working in a corporate office environment. The thought of working in an office environment makes me cringe while the thought of working a block from the beach makes me very happy.

If it doesn't work out at least I tried and I can start over again looking for a new job. I'm still young so there is not much to lose and if it works out then the credit card debt will be gone in no time.

Wednesday, April 12, 2006

All I have time to say is...

looking for a job is exhausting! I really feel like I need to be 2 people right now. I hope to have lots to blog about soon... and have the time to do it!

Thanks for all the good wishes. I was so worried I would have an angry mob of blogsters mad at me because I quit my job and the debt repayment would have to be on hold for a while. =)

Thursday, April 06, 2006

Bump in the road

I quit my job! It feels liberating and terrifying at the same time. I tried to look for a replacement job while I was still working at my current job but it was just too difficult. I don't know how people do it, trying to sneak phone calls in during business hours and making excuses to go on interviews. Regardless, I gave my two weeks notice and will soon be joining the ranks of the unemployed.

I kind of viewed my job as an abusive relationship. I knew it was bad for me but I depended on it to give me security and even though most days I was so stressed out that I could vomit (sorry for that mental picture), I was comfortable there. I tried to stick it out until I was debt free but 4 months seemed so far away. Before you get all up in arms let me make a few points:

1) What is more important? Being happy or being debt free? Being debt free will come in time but living your life in misery will have long term consequences. Think about how stress can take years off of your life and cause all kinds of diseases like heart attacks and stroke. I had to make the choice to take back my sanity and slow down the debt reduction for just a little while.

2) When I transferred my credit card balance to a card with a 0% interest I stopped making payments directly to my credit card (except for the minimum payment) and started socking the additional money into a high yield savings account. As a result, I have a 3-4 month reserve of cash that will tide me over until I find another job.

3) I am not paying any interest on my debt. I have until January of next year to pay it back without paying any interest on it. Even if I can't pay it back by next January I can always find another 0% interest offer to take advantage of. I'm not saying that is what I am planning on doing or that I would like to do it but if worse comes to worst it is a possibility.

4) There is a good job prospect that kind of fell into my lap the day that I gave my notice. If it works out, I could be working again right away and it won't affect the debt repayment at all.

5) Heaven forbid if I don't find another job in 3-4 months I can always go back to school full time.

I vow not to increase my credit card debt while I am looking for another job and still feel that I can reach my original goal of being debt free in 2 years. This will just make the journey that much more interesting!

Friday, March 31, 2006

My 0% interest scheme was a flop

A while ago I wrote about using a 0% balance transfer offer to earn a little extra money buy putting the transferred money into a high yielding savings account. There are technically no rules against this and although the interest would not be substantial (probably would amount to about $300), it would be "free money". I was ready and determined to avoid any sneaky fees that the credit card company might try to charge me. I was not ready however, for the endless delays that they would subject me to.

I called the credit card company and told them that I wanted to wire transfer $23,000 into my checking account. Unfortunately, the thing I did not know was that in order to request a wire transfer, you have to call from your home phone number. When I moved, I had failed to update the number on my account and the old number had long been disconnected. I updated the phone number and would have to wait another 30 days for the change to take effect. It was frustrating, but understandable. They were only trying to look out for me, right? She suggested that I simply write one of the checks and take it to my bank to deposit it.

That is exactly what I did. The only problem was that when I tried to deposit the check, they informed me that they would charge a $15 processing fee and would hold the check for 5 weeks to make sure it was legit. Apparently, banks have a dislike for checks from credit card companies. I fussed and fought but they were not budging. So I politely told them to shove it and left without cashing the check.

I waited and waited thinking of all the interest earning time that was passing by. Finally, I figured that it had been 30 days and called back to get my money. Everything seemed to be going fine. $23,000 is nothing to sneeze at so of course when I called and talked to the customer service rep they asked me to answer a number of security questions to verify that I was who I really said I was. He told me I should have my money in about a week. Finally!

Every day I would check my account online, waiting for the transaction to go through. Then one day I tried to log into my account and nothing was there. Panicked, I called them. They had placed my account on hold because they suspected fraudulent activity. (I know you can't see me right now but just imagine me rolling my eyes.) So I answer the security questions again and he cheerily informs me that my account should be back online in 30 minutes. Greeeaaat.

The next day, I log online and still nothing. I call back and go through the same ordeal.

Them: Did you recently initiate a balance transfer?

Me: Yes. I have already talked to two different people about this.

Them: O.k. ma'am. Well do to a high volume of fraudulent activity we need you to answer some security questions.

Me: Fine. But I've already answered these questions twice already.

After a series of exceedingly annoying questions, they confirm that indeed everything is legit (for the third time) and say that they will restart the balance transfer process and that I should get my money in a week. This is where I lose it.

Me: You told me a week ago that I would have my money in a week. Now you're saying that it is going to take another week?

Them: Well we had to put your transaction on hold because there were fraud concerns.

Me: Were you ever going to call and tell me this? Remember, I had to call you to solve this problem.

Them: We sent you a letter.

Me: A letter? I'll probably get that in a week. Couldn't you have at least called if you were seriously concerned about fraud?

Them: Um, we did. But we couldn't get a hold of anyone.

Me: Did you leave a message?

Them: Um, actually they said you didn't live there anymore.

I am so completely irritated at this point that I tell them to forget the whole thing. What was the point of me updating my phone number over a month ago if they can't even get the phone numbers straight in the first place? I won't even torture you with the back and forth exchange I had with these people about why they were calling the wrong number.

My theory is that they drag out the process as long as possible so you have the money at the 0% rate for a shorter amount of time. They used to give you 6 months or some predetermined amount of time to have the money at the lower interest rate. Now they do it so you only have it until a specific date. And not to mention that although they say that you have until say September 20th, they really mean that you have until September 20th or before the pay cycle that includes September 20th. This means that if you wait until September 19th to pay it back but your pay cycle begins September 18th, you are already too late.

It was a good idea but not made for a person with low tolerance for annoying customer service. I just couldn't stand the thought of having to call them and answer more security questions. Another victory for the credit card companies. But at least I don't have to sleep with the enemy anymore.

Thursday, March 30, 2006

Ever wonder...

what is the point of signing when you use your credit card? Does it really matter how you sign? Do you ever just get lazy and scribble your name? I always wished I had a cool doctor's like signature but alas, my signature takes me a good 15 seconds to execute. Every letter is clearly drawn, nice and neat. 15 seconds may not seem like a long time but it feels like an eternity when there are people practically pushing you out of line because they are in a rush to be next. These people clearly don't appreciate perfect penmanship. Would it really matter if I just quickly scribbled anything, just to seal the deal and get the heck out of the way?

Well, I happened across this funny article from Zug about someone who tried just that. Not necessarily because he (or she?) was in a rush but because (s)he wanted to see if people were paying attention. (S)he even went so far as signing with a grid and a stick figure. I got quite a laugh out of it. Next time I buy something with my debit card, I'll have to try it and see what happens.

Monday, March 27, 2006

Throw away the fashion mags

For a while I held on to the fashion magazines. I lived vicariously through the glossy pages, envisioning myself in the clothes or with the new lip gloss. I figured it was harmless because I wasn't actually buying anything but I was wrong. Really, I was just torturing myself with stuff that I wanted but could not have.

You see, I now look at fashion magazines the same way I look at malls. They are evil. Pure and simple. They are evil because they are loaded with ridiculously expensive things that alter your perception of what is affordable and what is not. My eyes nearly bug out of my head when I see the price tags of some of the items. $2,000 for a handbag, $800 for a pair of shoes, $550 for a sweater. It makes it so that when I see a pair of shoes for $220 I think they are a bargain! It builds us up to a false sense of practicality. Comparatively the $220 pair of shoes are a much better buy than the $800 pair of shoes so you are making a frugal decision, right?

Not to mention that fashion magazines are designed to make you feel, well, bad. Ever notice how in those "what's hot, what's not" sections, the what's not was what was hot last month? So now that you've run out and bought the latest trend you have to hide it in your closest or risk being passé and drag yourself back to the mall to buy what is hot this month. And the cycle repeats and repeats and repeats. You can never win.

Along with banning the mall I am now banning fashion and beauty magazines as well. I'm not saying that all magazines are bad. Just the ones that try to sell an impossible lifestyle. Magazines should be inspirational, educational and informative, not a test of willpower.

Maybe it's time to start subscribing to a personal finance magazine instead so I will be more tempted to save instead of spend!

Saturday, March 25, 2006

This is the thanks I get?

Last night I parked my car under a tree in front of my apartment. When I went down to my car this morning imagine my shock and horror when I found my car looking like this...

Keep in mind that when I left my car last night it was bird poop free. I looked around at all the other cars and not one of them had one drop of bird poop on them. I had parked in this spot and never had an incident like this before. Clearly, my car had been maliciously attacked by angry birds. They used the weapon they know best, their feces.

"Why?" you ask. I can tell you why those little buggers attacked my car. You see, it all started with trying to make my cat happy. We moved here from a place that was full of birds that my cat could watch from the window. Bird watching was her hobby. In our new apartment she had nothing to watch except a parking lot full of cars and the occasional person walking by. She was depressed and bored so I bought a bird feeder hoping that we could attract some birds to our balcony.

Months passed and no birds came. I tried everything to keep her happy. DVDs of birds, remote control mouse toys, I even contemplated getting another cat to keep her company. Nothing worked. Then one day I noticed that some of the bird food had been eaten and later I noticed that 2 little birds would come and eat out the feeder. My cat was finally happy.

2 birds turned into 4, 4 turned into 6 and soon I could have upwards of 16 birds on my balcony at any one time.

The birdy party crashers were eating me out of house and home. I would put food out when I got home from work and by the time I got home from work the next day the food would be completely gone. I went through a whole bag of birdseed in just one week. I tried to space out the feedings so that I wouldn't have to buy as much bird seed.

I ran out of bird seed and on my trip to the store I forgot to pick up more. I contemplated making a special trip but couldn't justify the effort for the birds. Apparently, the birds didn't like my decision. After 4 days of not having a refill, they decided to show me exactly how they felt about me.

You may be thinking that the bird poop happened because I had attracted these birds to my balcony in the first place. But I argue that I had never had a problem with a soiled car when they were regularly fed! Coincidence? I think not.

So I'm off to get an expensive car wash (I have not had any luck finding a cheap car wash around here) and some bird seed to mollify the angry birdy powers. I have learned my lesson.

Friday, March 24, 2006

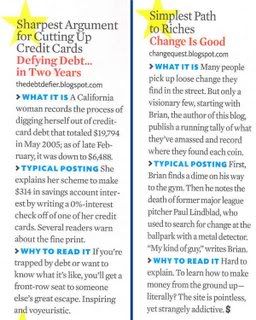

Blogs from the Financial Front

Hooray! They finally have the link up to the article at Money Magazine featuring the "Five online money diarists too smart--or weird--to miss". Am I the smart one? Or the weird one? Hmmm. ;) Regardless, I was pleasantly surprised to be mentioned along with:

Sound Money Tips

All Things Financial

Another F@cked Borrower

Change is Good

And thanks to Bailey from Thoughts from the Change Race for providing a scan:

Thursday, March 23, 2006

Bill Re-Evaluation

The whole fiasco with my auto insurance reminded me of the importance to re-evaluate all of my bills. It has been a while since the last time I really went over what all my monthly bills were and whether or not there were ways I cut back. So in the past week I have been doing some thinking and have decided on a couple of money saving sacrifices:

1) After comparing all of the auto insurance companies I decided that Unitrin was the most cost effective and reliable insurance companies, even with the additional $40 fee for renewing my policy. Even though I couldn't get that fee waived, after changing some of my coverages to what was more approriate (lowered bodily injury liability and dropped towing and rental car expense coverages) I was able to save $40 off of my premium.

They had also increased the per payment fee from $3 to $5. So I decided instead of paying on a monthly basis I would just pay for it all up front. This will hurt the debt repayment in the short term but after the initial hit I'll have more money per month to pay towards the credit card.

2) I cancelled my subscription to Audible. I don't commute anymore so I don't have any real need for audiobooks and I have a ton that I haven't listened to yet. That will save me $15 a month.

3) I changed my student loan repayment schedule from the most agressive repayment plan to the least expensive per month. That will free up an additional $50/month to put towards the credit card. While this may not save me any money (either way it would have gone towards debt) it will help me out mentally by speeding along the process of paying off the credit cards. Once the credit cards are paid off I'll be able to focus all of my energy towards paying off the student loans.

The end is near, I can almost taste it. The closer I get, the more excited I get and hopefully making these few small changes will help me along my way.

Getting to Know...Me

Head on over to the NCN Network to read a little email interview with none other than yours truly. Find out why I started to blog, what my long term personal finance goals are and much more than you ever needed to know about me.

Wednesday, March 22, 2006

My Day of Salvation

I tried to calculate the exact day that I will be out of debt based on my pay schedule and when my bills are due. Based on my calculations I should make my last credit card payment on August 4, 2006. This is assuming I don't receive any extra cash before then and I don't have any major unexpected expenses. That means that I have 162 days until I am debt free!

Tuesday, March 21, 2006

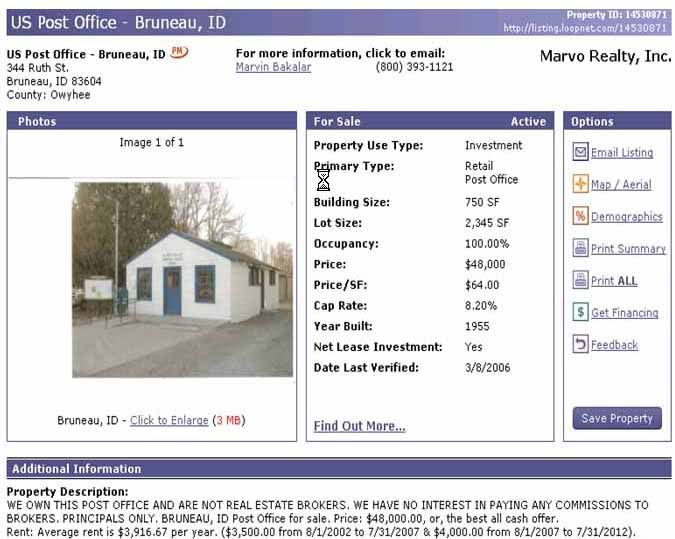

An unusual real estate investment choice

Tonight I sat in on a very introductory course on real estate investment. A lot of the stuff I already knew but one thing that struck me as unusual was one of the property types he suggested for beginners. In addition to the usual suggestion of purchasing a condo, a single family home, a multifamily home like a duplex, or a small retail space he suggested buying a post office.

I didn't even know that you could buy a post office. I assumed that the government would own the building and the land that they operate the post office on, but I was wrong. Anyone can buy a post office and lease it out to the U.S. government.

Think about it. What a sweet deal that would be! The biggest drawback that I have always envisioned for owning investment real estate is that you have to deal with people, people who don't pay their rent and who don't care about maintaining the property. If the U.S. government is your tenant most likely they are not going to be throwing wild parties and they will have the money to pay you rent (well, lets hope so because if they don't we're all in trouble).

Here are some of the advantages to owning a post office:

*Rent to a Stable tenant

The U.S. government usually signs 5 year leases so you are guaranteed the income for at least 5 steady years. Most post offices tend to stay in the same location year after year. When was the last time that your post office moved?

*Tenant responsible for all expenses

You won't have to worry about them running up the electric bill because they have to pay for it.

*Post offices are everywhere.

This means that there are plenty of cheap locations to choose from.

*Easy to manage.

Post offices are pretty self sufficient so there is no need to hire a property management company that will cut into your cash flow. Also, you can buy out of state and not worry about having to visit the property often.

A quick search on a commercial real estate search engine produces this affordable post office in Idaho. Only $48,000 to buy with an 8.2% CAP rate (rate of return on your investment).

So it all sounds good, huh? What are some of the disadvantages?

*If the post office decideds to not renew its lease, you'll have a hard time finding another tenant to replace them. If that happens you'll most likely be able to only sell it for its land value.

*It's hard to find financing.

*The U.S. government is hard to negotiate with. You'll have a tough time trying to raise the rents on them.

Not a bad deal if you ask me. It's better than having to deal with clogged toilets and evictions.

Sunday, March 19, 2006

What $300,000 + Buys You in…Orange County, CA

JLP over at All Things Financial started a post on what $300,000 will buy you in the real estate market in his neck of the woods and has encouraged other PF bloggers to do the same. O.k. I'm game...but can you really buy anything in Orange County (Irvine) for $300,000?

The answer is yes, but you're not going to get much! The closest thing I could find to $300,000 was this "spacious" 1 bedroom, 1 bath upper-unit condo of 643 s.f. for $299,900.

Now maybe you can understand why I feel like I will never own a home unless I move out of the state.

Just Say No to the Mall

The mall is an evil place. Walking into a mall is like walking into a vortex where your money is sucked straight out of your wallet, or even worse, money you don't have is charged to a credit card.

The mall is an evil place. Walking into a mall is like walking into a vortex where your money is sucked straight out of your wallet, or even worse, money you don't have is charged to a credit card.

O.k. Maybe I am being a little dramatic in saying that the mall is evil, but I definitely feel there is something sinister about a mall. The mall has a way of casting a spell over me while I am there. Things that I didn't even know existed are all of a sudden a necessity and my entire wardrobe seems helplessly shabby and outdated in comparison to the fresh new styles on the racks of countless stores. I lose all sense of rationality and my old mantra of "You only live once" creeps back into my mind and I feel tempted to go on a wild shopping spree. This is why I now avoid the mall at all costs!

You see, I think a lot of Americans end up in debt out of sheer boredom. Go to the mall on any day of the week, especially Saturday and Sunday, and you will find throngs of people filling the malls, fighting over parking spaces and bumping into each other with their baby strollers. Why are they there? Surely all of these people don't need to be there. I think many of them just can't find anything better to do than to hang out at the mall and grab a Cinnabon or a hot dog on a stick. And while they are there passing the time, they end up spending money that don't have on things that they don't need.

I remember every Saturday my grandma and her sister would go to the mall. It was a sort of ritual they had. Rain or shine, regardless of whether they needed anything or not, we would all go to the mall and then go out to lunch afterwards. It's only now that that strikes me as bizarre.

I rarely go to the mall anymore and I've found that my desire for things in general has dropped considerably. For the most part I am content with what I have and can resist emotional or impulsive spending. Sure there are times when I feel the need for something new but its much easier to resist when I am far, far away from the mall.

So if you are in debt or are trying to save money, stay away from the mall. I suggest having a healthy fear of the mall. Think of it: rabid frenzied women pushing you out of the way to get to the big sale, no parking, bad food, and worst of all...money being sucked right out of your bank account, never to be seen again. Not my idea of a good time!

Saturday, March 18, 2006

How Much Car Insurance Do You Really Need?

I've been with Unitrin Direct auto insurance for the past year. They were the cheapest quoted when I went to www.insurance.com and when I switched to them from Mercury insurance I saved about $40 a month. I've never had any really problems with them...until now.

I received my renewal package in the mail and was looking through it to make sure they hadn't raised my premium and was even hoping they would decrease my premium. Neither really happened but what they did do was slap on a $40.00 "policy set up fee" to the total bill. What? A policy set up fee? Nothing on my policy had changed, nothing fancy is required of them. And to make things worse, they decided that they are no longer doing annual policies but instead are now only offering 6-month policies so in another 6 months when my policy renews I will have to pay another $ "policy set up fee." What BS!

Their policy set up fees will end up costing me another $80/year or about $6.60/month. I hate when companies nickel and dime you so that they can lure you in as customers and then try to squeeze as much money out of you as possible. It's more than principle of the matter more than anything. Why not include their expense costs in the premium instead of making it seem as if they are doing you a favor or providing you some additional service by renewing your policy? Isn't that exactly what their business is?

I called them and told them "NO THANK YOU" to the additional fees and they said "TOUGH LUCK." So I started shopping around for auto insurance.

I went back to www.insurance.com and got back a few different quotes, only 1 of which was less expensive than the quote at Unitrin. Annoying but the quote that was less was $108 cheaper for a 6 month policy than at Unitrin. All of the other quotes were

The quote was from Esurance so I decided to do a quick search to see what they were all about. I was so glad I did because I read numerous complaints from the Consumer Affairs website about them claiming that they gave them the run around when they submitted a claim or that they ended up raising their rates during the policy period for no good reason. I think I'll take a pass on them.

Here is what I don't get. I'm 24, never been in an accident, never had a ticket, have a good credit rating and only drive 4 miles one way to work. My car is pretty reasonable; it's about 3 or 4 years old, I own it and it is probably worth about $13,000. But for some reason I end up with ridiculously high quotes from insurance companies. AIG gave me a quote of something like $1,100 for 6 months or $183/month. That could be another car payment!

Maybe its time to reevaluate my coverages. There could be other ways to trim down my auto insurance cost which is my biggest expense after rent, credit card payment and student loans.

I found a good article on this subject at Smart Money. Here it is in paraphrase form with some of my own comments. I recommend checking out the full article as well.

Bodily Injury Liability

This will compensate the driver of the car and its passengers and passengers in your car when you get into an accident. The amount of coverage you need should be determined by the amount of assets you need to protect. This was news to me. I had bodily injury liability coverages of $100,000/$300,000 and I don't even have any assets besides my car. Unless they want to take me to court to win a portion of my credit card debt, I should really lower my coverages here. Smart Money recommends using their Net Worth calculator to determine the amount of assets you need to protect.

Property Damage Liability

This will help pay for the cost of damage to the other party's car. If you live in Orange County like me where too many people buy ridiculously expensive cars, you should have enough to cover the cost of that Mercedes or Porsche.

Personal Injury Protection

This will cover medical and funeral costs of you are passengers in your car regardless of whose fault it is. If you already have medical & life insurance you can be fairly safe in skipping on this coverage.

Uninsured or Underinsured Motorist

This will cover medical and funeral cost for you and your family if you get hit by a hit and run driver or with someone without any or enough auto insurance. A definite because of the number of people driving without insurance. It will make up for anything your medical insurance does not cover.

Collision and Comprehensive

Collision will reimburse you for the cost of replacing or fixing your car after an accident. Comprehensive will reimburse you for the cost of replacing or fixing your car in the event of a natural disaster, theft, or vandalism. It's best to choose the highest deductible available (usually $1,000) so that you can save on the amount your policy premium will cost you. In the long run, you'll only be paying more than $500 to reduce the amount of deductible you have. This is only of course, if you'll be able to pay the $1,000 deductible if you are in an accident.

If you have an older car it may make more sense to drop collision and comprehensive all together as these coverages can make up 30-40% of your total policy cost. If you get into an accident the amount of money you receive to replace or fix the car may not be more than you have already paid in insurance.

Car Rental and Roadside Assistance

The likelihood that you will need to use them are pretty slim. You'd be better off paying for them out of pocket if you do need them instead of paying a monthly fee just in case you might need them.

Unfortunately, even taking into account some of these changes, I still can't find a price that beats Unitrin and isn't shady like Esurance. It would be nice to move to a more reputable company like Geico or 21st Century but I would have to pay at least $40 more per month. In the end I just don't feel it is worth it. I guess I'll have to keep crossing my fingers and hope I don't get into an accident. And it gives me a reason to look forward to getting older...maybe when I turn 25 I'll start getting lower auto insurance rates!

Thursday, March 16, 2006

When you love your shoes too much...

I have a confession to make. I'm not really a shoe person. I'm one of those people that would walk around bare foot or in flip flops most of the time if I could. This works out great for me because I am not tempted like some people to spend an inordinate amount of money on shoes thus breaking the budget. I have other vices but shoes are not one of them.

Mainly I hate shoes because they tend to hurt my feet, especially heels. I've never gotten used to walking in heels and I always look ridiculous when I do. Just today, I tripped and nearly fell on my face 3 (yes three!) times because my heels got stuck on something or I twisted my foot the wrong way. Its fine as long as no one notices. I usually do a quick look-around to make sure no one saw and if I don't see anyone giggling then I'm cool. But its hard to play it off when you are trying to carry on a conversation with someone and all of a sudden you are immobile and your shoe flies off of your foot because it has gotten stuck in the floor (and yes, this did happen to me today).

I'm just not one of those girls who freaks out about shoes and wants to own 100 pairs of Prada or Jimmy Choo shoes. I have a hard time getting excited about shoes because I know that my feet will hate them and its hard for me to care how cute the shoes are when I'm in excruciating pain and falling all over the place. Even tennis shoes are hard to buy because it is so difficult to know whether or not they are going to be comfortable because they have to be broken in before you can truly know the nature of the shoe.

But alas, there is one pair of shoes that have always done me right. I bought them about 5 years ago and never regretted the $80 I spent on them. They carried me across Europe on a backpacking trip and I wore them just about everyday when I was in school and didn't have a car and walked everywhere. When I wear them I feel like I'm not wearing anything at all and they provide great ankle support so I can really hussle when I'm walking somewhere in a hurry.

They have looked terrible for a while now but I can't bare to part with them. I've washed them but they still look dirty and there are little plastic things that are falling off left and right.

I've bought other shoes since then but they don't compare. I feel like every time I buy another pair of shoes I am just wasting my money because I won't want to wear them. On the other hand, I don't want to wear the old shoes because they look beat. There comes a point when frugality must make way for fashion.

So what is a girl to do? I either buy new shoes which could be a waste of money (and money is tight) or I can just keep the old shoes and look, how do you say, ghetto.

I did have one other brilliant idea. I could just try to find the same old shoes for sale on the internet. Unfortunately, these shoes seem to be a rather rare find. I searched through tons of shoe listings on ebay but didn't have any luck finding the shoe.