What did 2005 teach me?

1) Determination can accomplish anything.

You cannot be crippled by overwhelming situations. The only way to change things is to take a deep breath, develop a plan, and stick with it. It's been hard; it's been a pain but that will make it way more satisfying when I am finally debt-free.

2) Support makes the journey more bearable.

I want to thank each and every one of you who visit this site and offer words of encouragement and advice. Before I started this blog I felt all alone. My debt was a dirty secret that I didn't want people to know about and the loved ones that did know about it couldn't relate. It has been great to read about people going through similar situations and learning from them as well as being held accountable for my own progress.

3) Keeping track of your finances electronically only works if you keep a back-up.

After my laptop died in July, I lost all of my financial info that I saved in Quicken. Oops! I learned you need to keep a copy somewhere other than your hard drive. I wanted to be able to do a year in review but I'll have to make due with what I have.

4) Don't expect to get the raise you deserve without asking.

I posted here before about my 4% raise but I didn't post about how they increased my raise to 9% when they feared me leaving for another job. I was a bit jaded along with a few other employees; word got around and well they increased my raise. I wasn't happy with how it happened. I should have told them straight up that I thought I deserved a bigger raise without all the drama that ensued from me not speaking up. It wasn't a monumental raise but it was easier than finding a new job. Lesson learned.

5) Consolidate student loans early.

I didn't look into consolidating my student loans until after it was too late. I thought since I only had one payment that I didn't need to worry about it. Alas, I was wrong and if I had consolidated just a few weeks earlier I could have locked in a smaller interest rate.

6) Commuting is a waste of time and money.

I am so glad I made the decision to move closer to work. I don't have as much money to pay back towards my debt but I am able to make it worth it by cutting down automotive related expenses (gas, maintenance, depreciation), working more overtime, and being able to go back to school to increase my earning potential. Plus, eventually I would probably eventually run up lots of medical bills with stress related illnesses.

7) PPO is not the right option for me.

Some people really like having a PPO. It is nice to be able to go to almost any doctor you want, when you want until you have a major medical catastrophe and you are responsible for 20% of your medical expenses. I never knew how much X-rays, diagnostics tests and hospital stays could cost until I had to pay 20% of them. As soon as I was able to, I switched to an HMO.

2005 was a good year for me. Here is what I was able to accomplish:

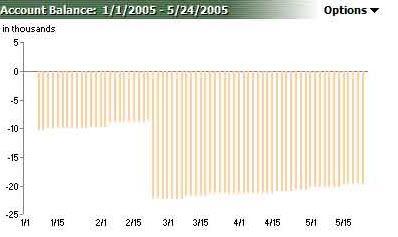

1) Since the beginning of the year I have paid off more than $13,000 of credit card debt. I wasn't able to create a comprehensive graph showing the progress but I found this old graph from one of my first posts:

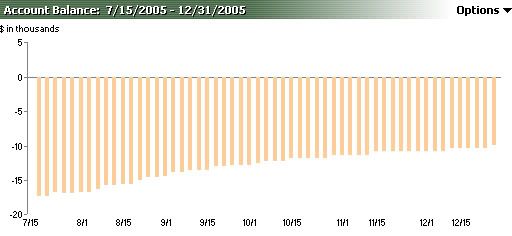

and a new graph that shows my progress from July 2005:

The spike in the first graph comes from when I transferred my car loan to my credit card using a low interest balance transfer check. So in 2005 I consolidated my credit card and auto loans and reduced the amount of interest I was paying every month while making it easy to aggressively pay down the debt.

2) Paid off $1,250 of my student loan debt. Not a huge amount because I was focusing most of my energy to the credit card.

3) Saved nearly $2,000 for retirement in my 401k. Again, not a lot but it is something. Next year I will be 20% vested in my company's matching so I will have even more.

4) Weathered a major medical expense without having to rely on credit cards. Who knew that having an appendix taken out could result in more than $2,000 in medical expenses? No more PPO for me.

5) Moved out of the family home and got my own apartment. Bought furniture and all the other comforts of home without having to put a single dime on my credit card.

All in all this year has been most productive and I feel it can only get better in the future. Here are my New Year's Resolutions for 2006:

1) Pay off credit card by September 1, 2006.

This will require me to pay a little more than $1,000 towards my debt every month. Right now I have been having a slightly difficult time finding the $1000 to pay every month but I think I can do it if I try harder.

2) Continue to save for retirement and stay at my job until I have at least reached the 20% vested mark.

3) Go back to school and complete at least two courses that I think would be interesting and beneficial for my future.

4) Once the credit card is paid off, focus on the student loans with as much intensity as the credit card.

5) Learn more about investing.

6) Increase savings in both savings account and CDs.

I find it almost therapeutic to look back on the year, both at what went wrong and what went right. It's by learning from our past mistakes that we grow to be better in the future! Hope everyone has a safe and prosperous 2006!